The Debt That Feeds On Itself

Why runaway government debt, stagflation, and political paralysis are creating the most favourable environment for physical precious metals in a generation

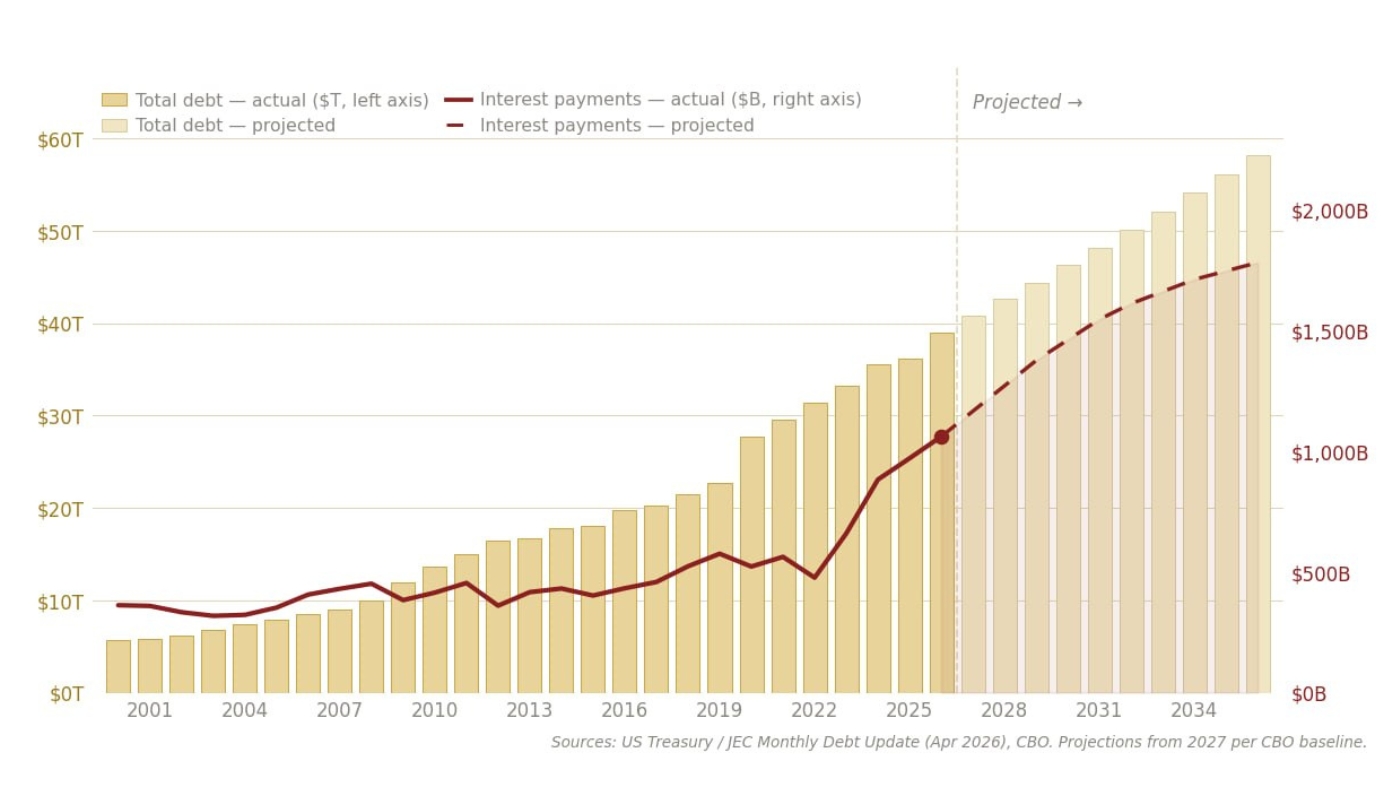

The United States has crossed a threshold that should concern every investor, regardless of where they live. For the first time in history, annual interest payments on the national debt have surpassed $1 trillion — more than the entire defence budget, more than any other single item in the federal accounts.

This is the nature of a debt spiral: deficits require new borrowing, new borrowing carries interest, interest swells the deficit, which requires yet more borrowing. The loop is self-reinforcing and, at this scale, very difficult to break.

What makes it particularly striking is that there appears to be no political will to even try. The US Congress recently tucked $1 billion in taxpayer funding for security upgrades to a presidential ballroom — a project originally promised to cost nothing to the public — inside an immigration enforcement bill. How can USD 1,000,000,000 be spent on ballroom security while the country pays a trillion dollars a year just in interest on its debts?

The answer lies in an attitude that has defined US fiscal policy for decades. When Treasury Secretary Paul O'Neill warned Vice President Dick Cheney in 2002 that deficits were becoming dangerous, Cheney's reply was unambiguous: “Reagan proved that deficits don't matter. We won the midterms. This is our due.” That philosophy has governed both parties ever since. The bill is now arriving.

The debt problem is not uniquely American — Japan, the UK, France, and many other governments carry debts at or above their annual economic output. But the US dollar remains the world’s primary reserve currency, meaning that US fiscal choices ripple through global bond markets, currency values, and commodity prices everywhere.

When the largest sovereign borrower in history loses its fiscal anchor, the consequences are global. The arithmetic of resolution is grim. There are only three possible exits — and none of them are painless:

|

||

|

||

|

II. The Stagflation Backdrop

Compounding the debt problem is the inflationary environment. In our recent newsletter on stagflation, we outlined how the combination of trade tariffs, Middle East energy disruptions, and supply chain deglobalisation is creating persistent price pressures that central banks cannot easily address with conventional tools.

Raising rates controls inflation but accelerates the debt spiral. Cutting rates feeds inflation. The central bank has no good options to solve a problem created by decades of irresponsible fiscal policies. And when a debt spiral spins out of control at the same time as the supply of real goods is constrained, it is like pouring petrol on a fire — monetary excess meeting physical scarcity, with predictable consequences for prices.

Political pressure intensifies the problem further. The Federal Reserve — whose independence is central to any credible inflation-fighting mandate — has faced unprecedented executive branch pressure to cut rates regardless of inflation data.

When a central bank cannot do its job freely, the most likely outcome is that nominal rates stay lower than inflation warrants. The result: negative real interest rates. And negative real rates, as history consistently demonstrates, are the most powerful environment possible for gold and silver.

III. The 1970s: What Actually Happened

The closest historical parallel to today’s combination of fiscal deterioration, supply-driven inflation, and politically compromised central banks is the stagflation of the 1970s. Two distinct oil shocks — the 1973 OPEC embargo and the 1979 Iranian Revolution — delivered the energy component. Dollar debasement, following the end of the Bretton Woods fixed exchange system in 1971, removed the monetary anchor.

Major central banks repeatedly fell behind inflation rather than confront it decisively. The environment that followed was damaging for conventional assets and transformative for gold.

|

Gold Performance · Two 1970s Stagflation Episodes |

|||||

|

|||||

|

Gold rose from $35 per ounce at the start of the decade to $850 by January 1980. Silver posted similarly dramatic gains across both episodes. Stocks and bonds delivered negative real returns across the full period. Crucially, gold did not simply rise as a crisis trade — it sustained its advance over years, as the underlying monetary and fiscal conditions remained unresolved.

By the late 1970s, gold had become a mainstream allocation. Central banks that had dismissed it as a relic were reconsidering. Private investors globally — from Europe to the Middle East to Southeast Asia — were buying in volume.

The shift from fringe asset to consensus holding happened gradually, then rapidly. Those who had established positions early, before that consensus formed, captured the majority of the gains. The same dynamic is beginning to play out today, with central bank gold purchases at multi-decade highs and institutional demand building across Asia, the Middle East, and Europe.

|

Key difference from the 1970s The 1970s ended when central banks were finally permitted to raise rates aggressively enough to generate positive real returns. Today, with debt loads being much larger relative to the economy than they were then, that exit is far more difficult. A Volcker-style rate shock would add trillions to annual interest bills across major sovereigns. The inflationary resolution is therefore more likely to be prolonged — and the case for gold correspondingly stronger for longer. |

IV. Physical, Not Paper — And Why It Matters Now

The case for gold and silver is well understood. Less understood is why the form of ownership matters as much as the decision to own. In the environment we are describing — sovereign debt stress, inflationary financial repression, and potential systemic strain in paper markets — the distinction between physical metal and paper claims on metal becomes critical.

Gold and silver ETFs, unallocated accounts, and futures contracts are financial instruments. They provide price exposure, but they do not represent ownership of specific physical metal. In a stress scenario — a bank failure, an exchange default, or a liquidity crisis — these instruments are subject to counterparty risk, settlement risk, and potential restrictions. This is not theoretical. The London silver market has experienced episodes of acute physical tightness where the gap between paper prices and physical availability became meaningful. In our recent supply updates, we documented how exchange inventories at the SGE, LBMA, and COMEX have declined significantly, while institutional premiums for physical metal have risen.

Legal title ownership of specific physical metal — stored in your name, independently audited, and insured through Lloyd's of London underwriters — does not carry these risks. It is not part of anyone’s balance sheet. It cannot be hypothecated by others, lent out, or caught in a clearing system failure. It is yours, unambiguously, regardless of what happens in financial markets around it.

The right time to establish that position is before the trends we are describing play out in earnest — before physical scarcity becomes the headline, before the premium between paper gold and deliverable gold widens to the point where the distinction is obvious to everyone. At that stage, the options narrow considerably. The advantage of physical ownership is precisely that it removes you from that uncertainty entirely, before it arrives.

Regards,

Gregor Gregersen

Founder & CEO of Silver Bullion Pte Ltd