What is a Parcel?

A parcel is uniquely identified physical property, audited, fully insured, guaranteed to be genuine and subjected only to Singapore law. Parcels can be securely stored long-term, traded near spot prices, taken delivery of or collateralized to obtain Secured Peer-to-Peer Loans.

Parcel Tracking and Auditing

Our S.T.A.R. Storage system was built to create and manage individual parcels and is integrated with our accounting system to reliably track the complex interactions between invoices, purchase orders and parcels over time. The system was later upgraded to incorporate DUX Testing (2012) and Secured P2P Loans (2015).

A parcel based segregated ownership system is inherently transparent and, to an extent, self-auditing because customers have great insight into the assets they own. They can check their ownership against the parcel ownership list which serves as the master record for all parcels and is made available to all customers. Furthermore, the traceability of parcels through documents means that any potential mistakes will be quickly spotted by staff, customers or auditors and corrected. This creates powerful checks and balances, resulting in a reliable and stable system.

While systems whereby bullion ounces are owed (IOU) tend to be black boxes - akin to a bank in that funds are not traced individually and they are legally owned by the bank - the S.T.A.R. Storage functions more like a blockchain as each parcel is tracked from creation to delivery with documents issued to certify parcel events such as a change of ownership or physical movement of a parcel.

This is best illustrated by understanding a parcel's life cycle and the corresponding documents created:

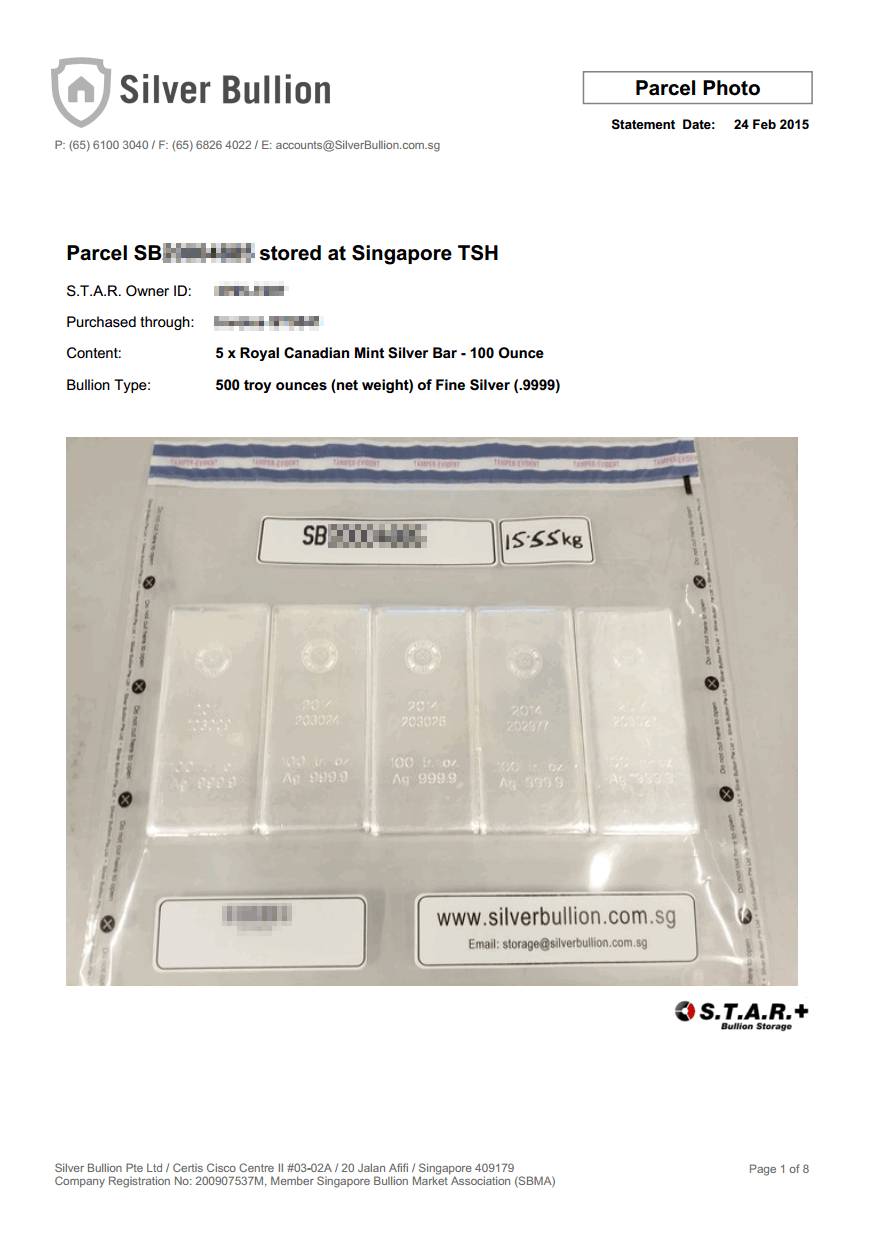

- A parcel must first be created from existing Silver Bullion inventory. The parcel creation process includes a photo of the parcel being taken and uploaded (Doc4) and may also include a DUX genuinity test (Doc5).

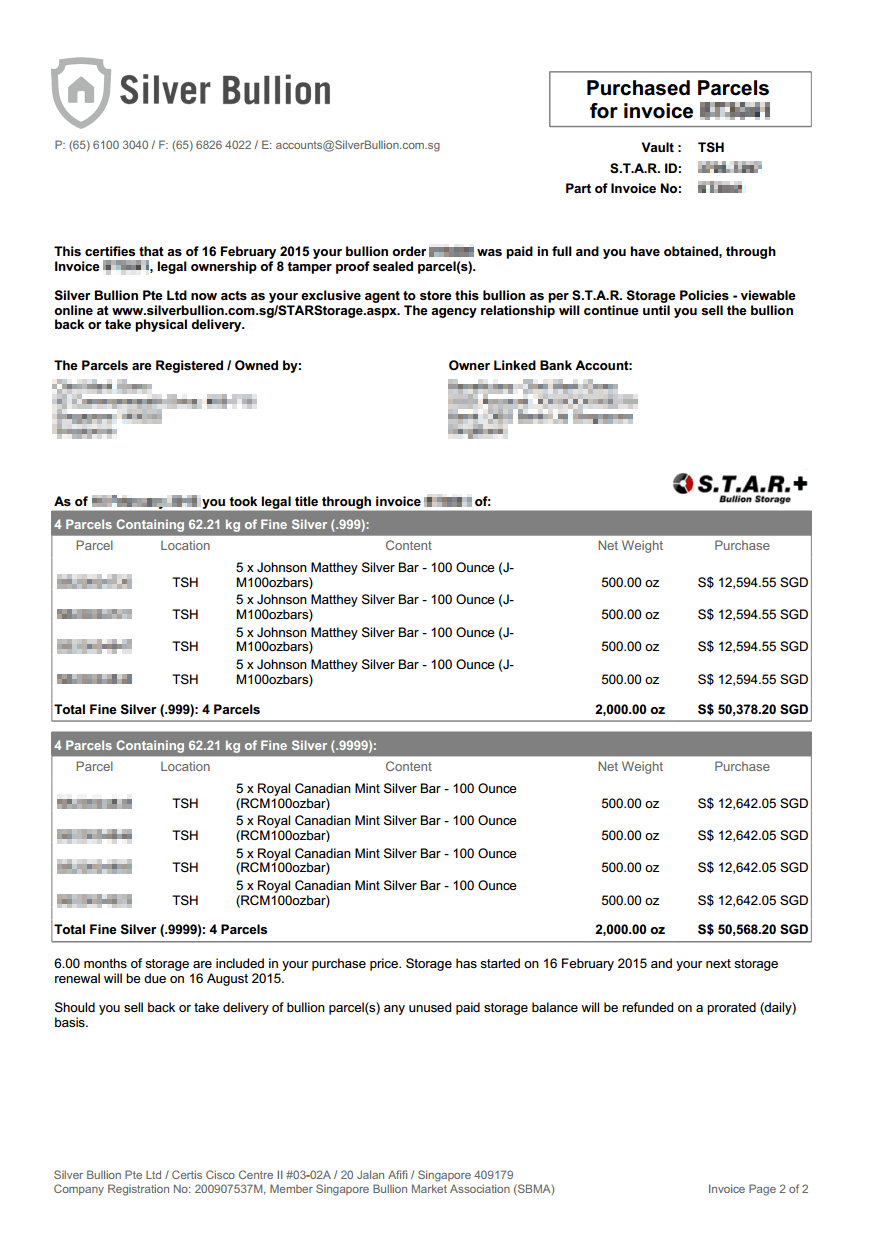

- The specific parcel is then sold to a customer via an invoice (Doc3) which evidences the transfer of parcel ownership and removes the parcel from Silver Bullion's inventory.

- The issuance of invoices and purchase orders in turn updates the Parcel Ownership List (Doc1), both will later be audited by third party auditors (Doc2).

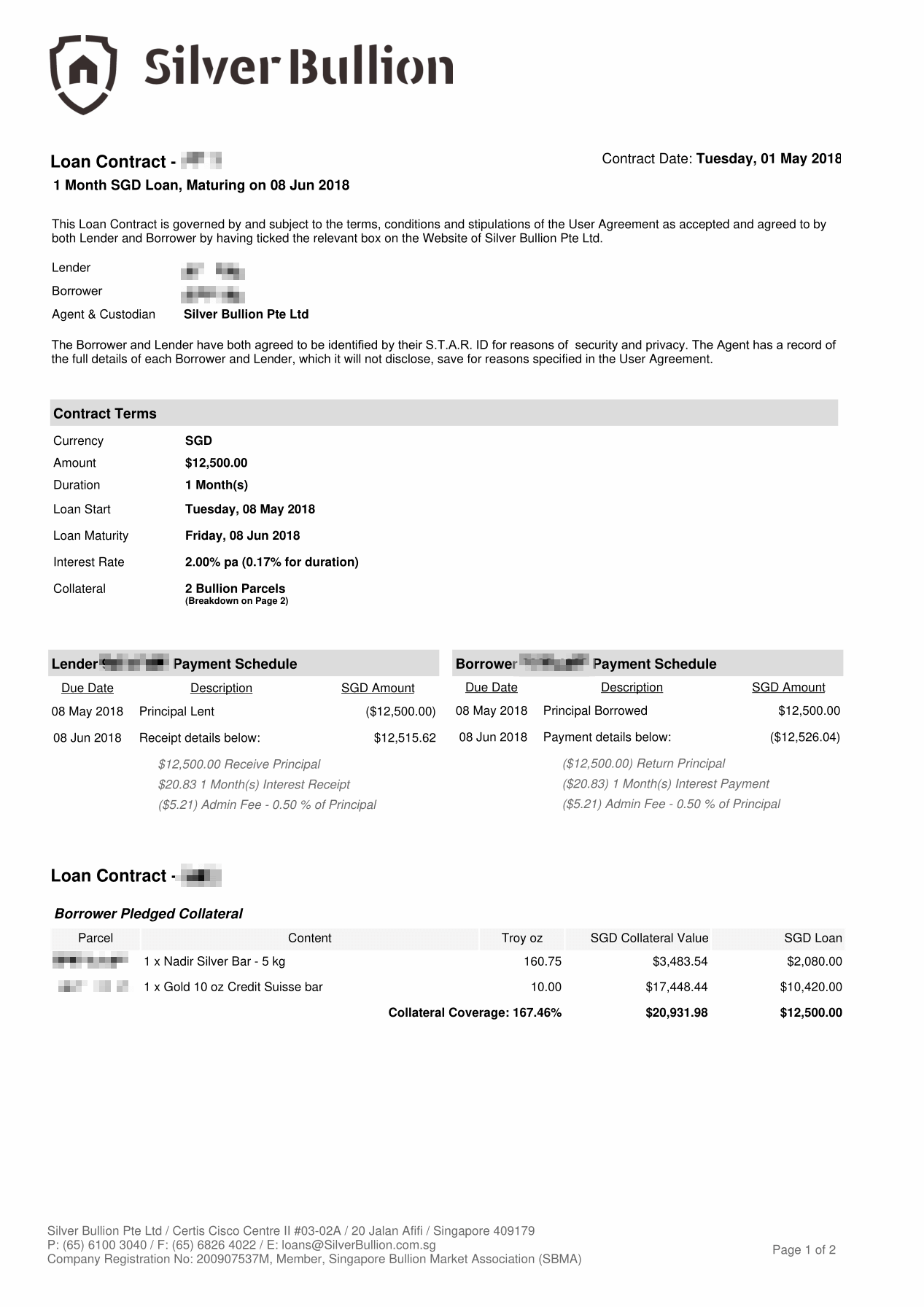

- Should the parcel be used as collateral in a lending contract (Doc6) the Parcel Ownership List will also reflect the loan contract number next to the parcel (Doc1).

- If the parcel is sold back to us a Purchase Order (Doc3) will reflect the transfer of ownership back to Silver Bullion inventory in return for payment and the Parcel Ownership List is updated (Doc1).

- The parcel can then be resold using a new invoice; or eventually the parcel's life will end when it is taken delivery of or withdrawn by an owner.

The following is a list of sample documents, each listing affected parcels, and their purpose.

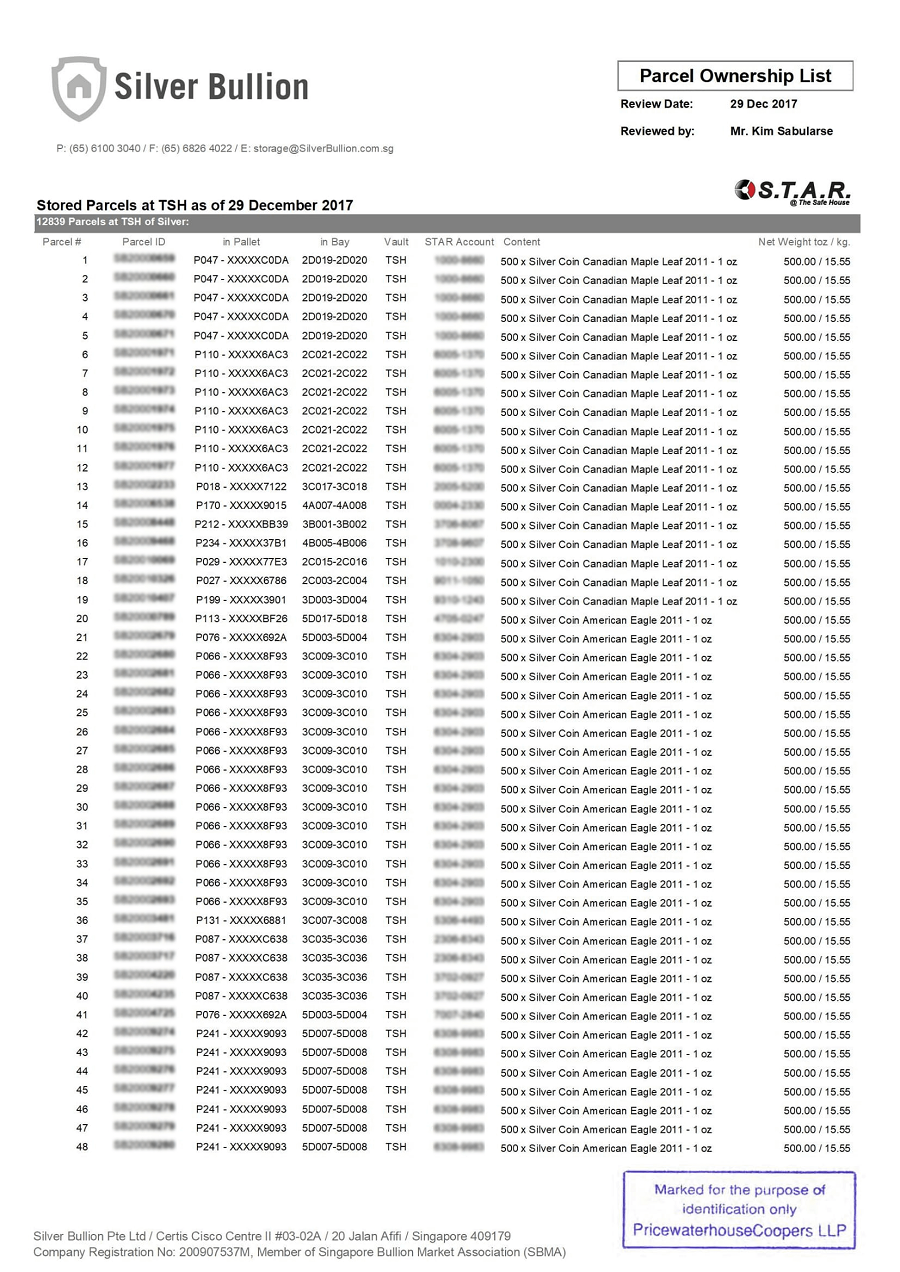

Lists all parcels and their respective eight digit S.T.A.R. Owners for a given date.

It ensures transparency as it is made available to all customers preventing a given parcel to be sold to multiple customers.

A parcel's ownership is transferred via an invoice or a purchase order (PO).

Issuing an invoice or a PO updates the Parcels Ownership List. Records are audited by our financial auditor.

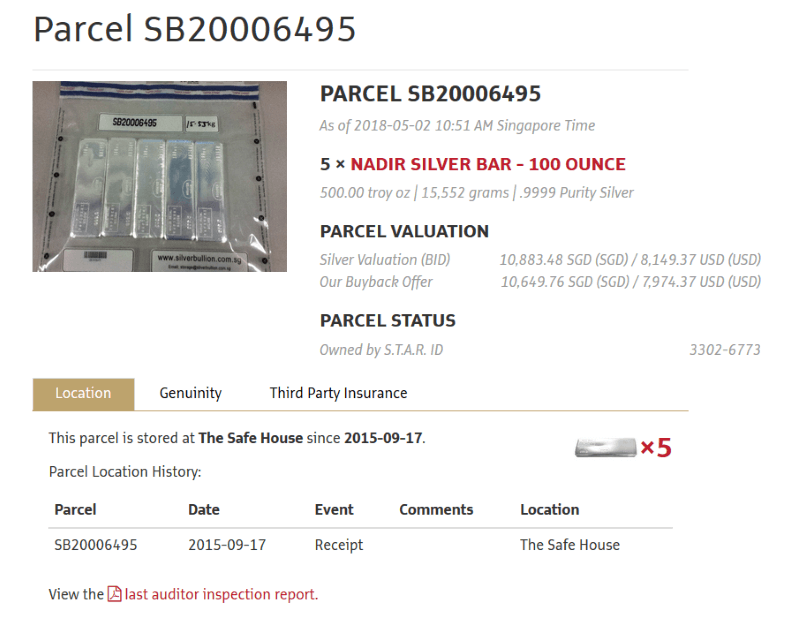

Displays a photograph of each parcel owned and details such as type of metal, purity, mass and the invoice the parcel was purchased with.

lists the parcels used as collateral for a given loan. Collateralized parcels cannot be sold or taken delivery of for the duration of the loan.

Once a loan has been repaid the parcels are unlocked and released.

While our financial auditors maintain a great reputation, it is the parcel tracking and the associated interested parties for each transaction that make the system strong. Interested parties are:

- Our staff, including the company comptroller whose primary task is to reconcile transactions.

- Customers who naturally check their Invoices, Purchase Orders, P2P Loan Contracts and possibly their parcels on the Parcel Ownership List.

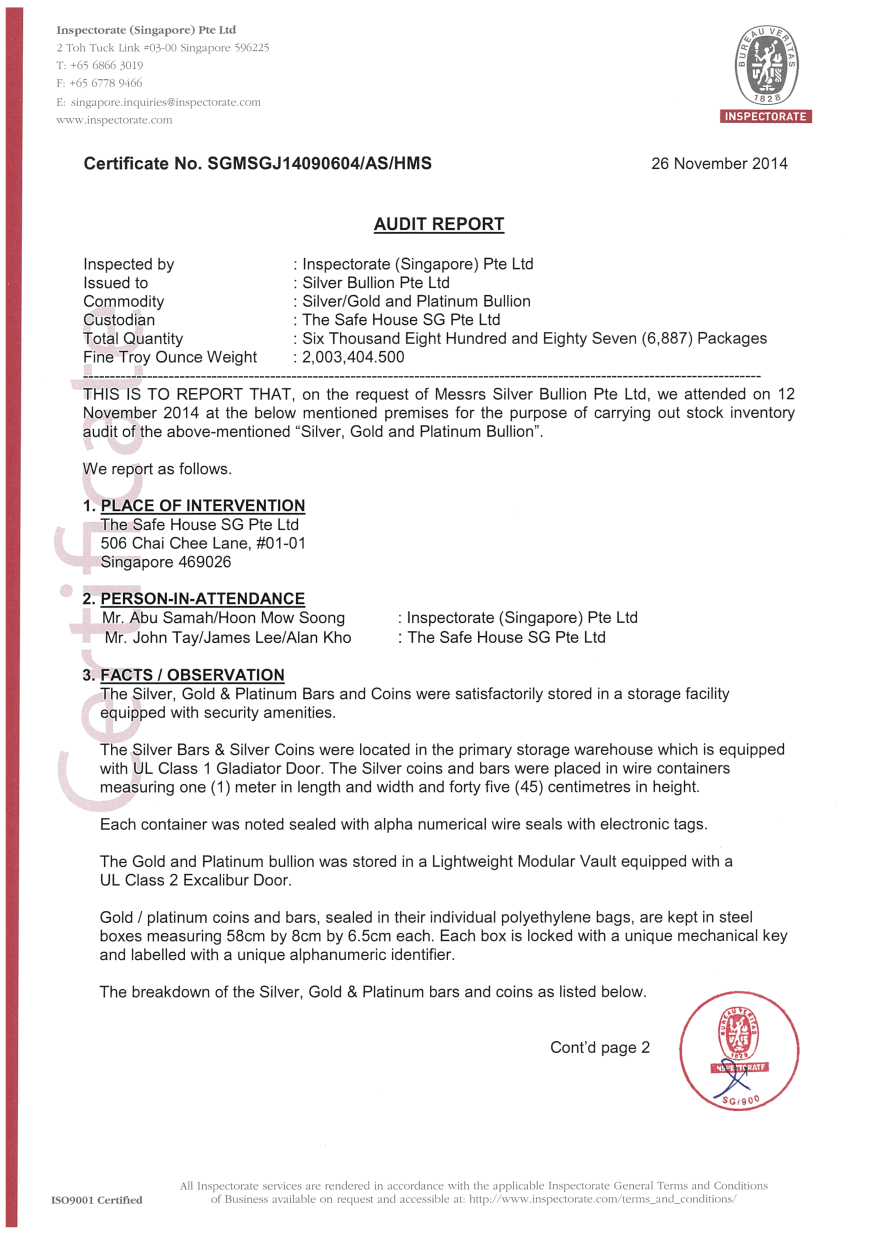

- Bullion Auditors, who are hired quarterly to physically inspect parcels against the Parcel Ownership List.

- Financial Auditors, who do a much more thorough check reconciling the company's books, invoices, PO and physical parcel audits.

Custom Audit Option

Additionally a custom audit can be arranged. Custom audits can be conducted either by a customer or by nominating a trusted representative and would involve a visit to the vault in Singapore and retrieval of a parcel properties to be audited. A minimum audit charge will be due.

Drilldown Interface Examples

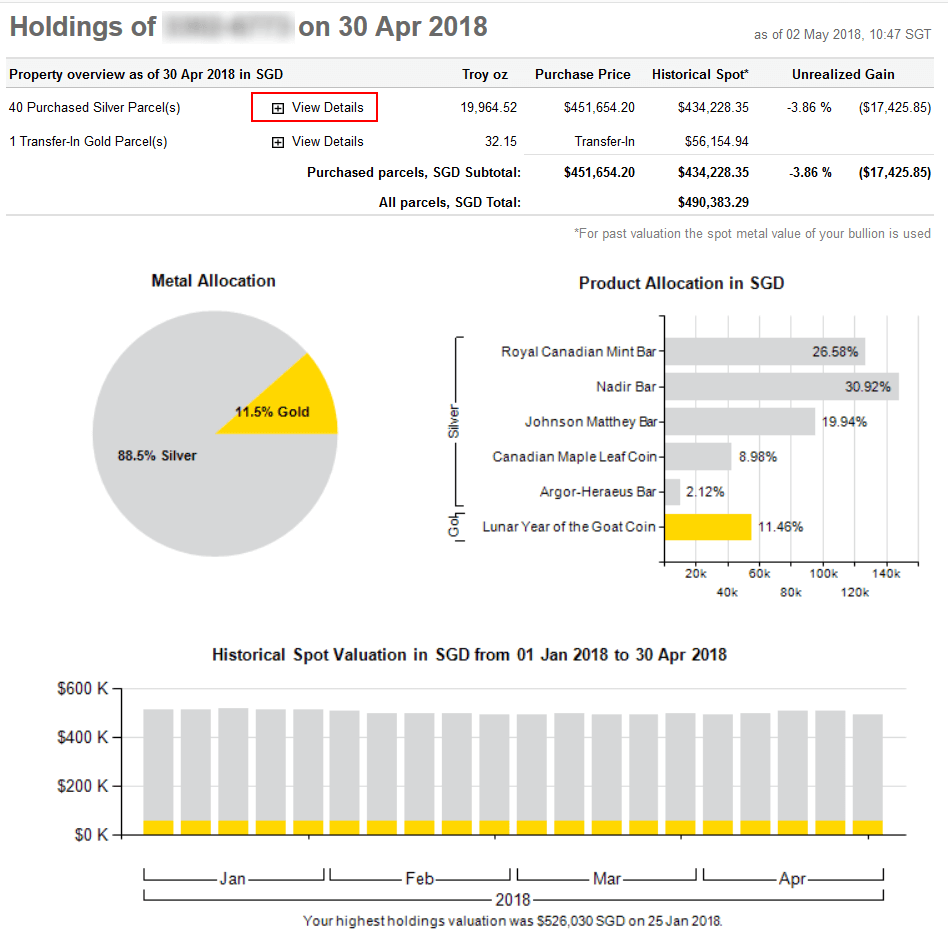

The sample "Holdings Overview" screenshots below illustrate the amount of transparency provided when tracking your parcels.

A typical holdings statement lists and aggregate number of ounces (e.g. 19,964.52 oz) at a given date. This is a typical report for both IOU and parcel systems.

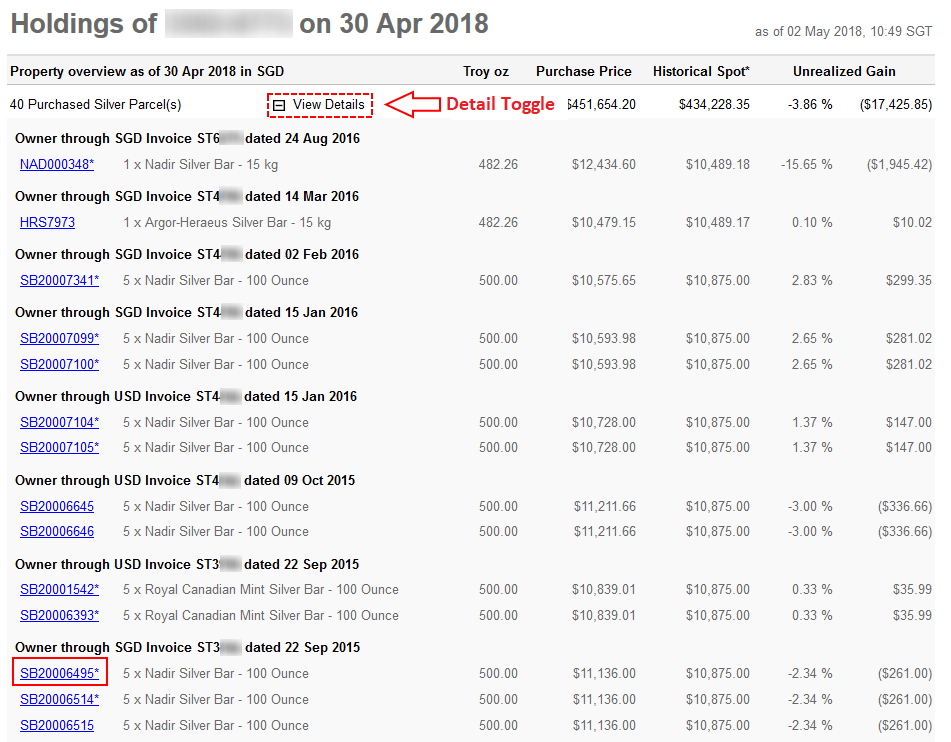

Details how each parcel contributes to the Aggregate numbers and lists invoices and prices. Invoices are checked by customers, auditors and ourselves.

Each parcel can be viewed to review its history, audit reports, optional DUX verification reports and insurance details, providing excellent transparency.